Economic Sanctions and the Nuclear Issue: Lessons From North Korean Trade

On September 14, North Korea conducted another test of its Hwasong-12 intermediate-range ballistic missiles (IRBM), flying over Japan for a second time within a month. This comes on the heels of the North’s sixth nuclear test, the largest it has conducted to date and commonly believed to have been a thermonuclear device. In addition to the political and technical implications of these events, this steady stream of testing continues to destroy devices presumably worth millions of USD by a country that, by all accounts, is having major economic difficulties.

The latest tests have once again intensified the international debate on how to respond to such events. Knowing military actions could have devastating results, discussion of response options quickly falls back on finding a stronger formula for economic sanctions to stop the funding stream to North Korea’s WMD programs. When considering new sanctions measures, it is important to understand three main issues: Where does North Korea get the money for its weapons program? Why have sanctions been unable to stop them? And will more sanctions, for example a ban on the export of oil to North Korea, be effective in curbing the North’s nuclear WMD development?

An informed discussion of these questions requires knowledge of hard facts. Unfortunately, these are particularly difficult to acquire in the case of North Korea. Among the few regular sources of information are the annual reports of Pyongyang’s state media on the state budget and the annual KOTRA reports on North Korean trade. Needless to say, both documents should be taken with a good grain of salt; we are in the middle of a propaganda war, and truth is a quick and easy victim in such cases.

But in particular, the trade data do not only suggest that sanctions have not worked so far; more importantly, they show that sanctions are unlikely to produce the desired results in the future even if they are tightened further. If this analysis is true, it is time to find a new strategy.

The North Korean Perspective

The country has made progress but is still far away from achieving its often ambitious economic goals. In his speech at the Parliamentary session in April 2017, the North Korean Prime Minister admitted that his country was experiencing difficulties in the field of electric energy, and that the dependency on imports of oil was a major strategic problem. Despite Chinese announcements of a drastic reduction of the import of coal, the North Koreans declared their determination to increase the production of anthracite, which points at more domestic use of this resource.

In the same report, the Prime Minister hinted at the support of the North Korean state for the production of consumer goods, which is an indicator of moderately growing wealth among at least a part of the population. People who fight for survival are not primarily concerned with shoes, household appliances or electronic gadgets. The Prime Minister’s remarks on agriculture supported the impression of an economy that is still poor, but not in crisis anymore. Rather than stressing the need to increase the production of staple food, he promised an increase in the production of higher-quality products such as meat, milk, fruits, mushrooms and vegetables.

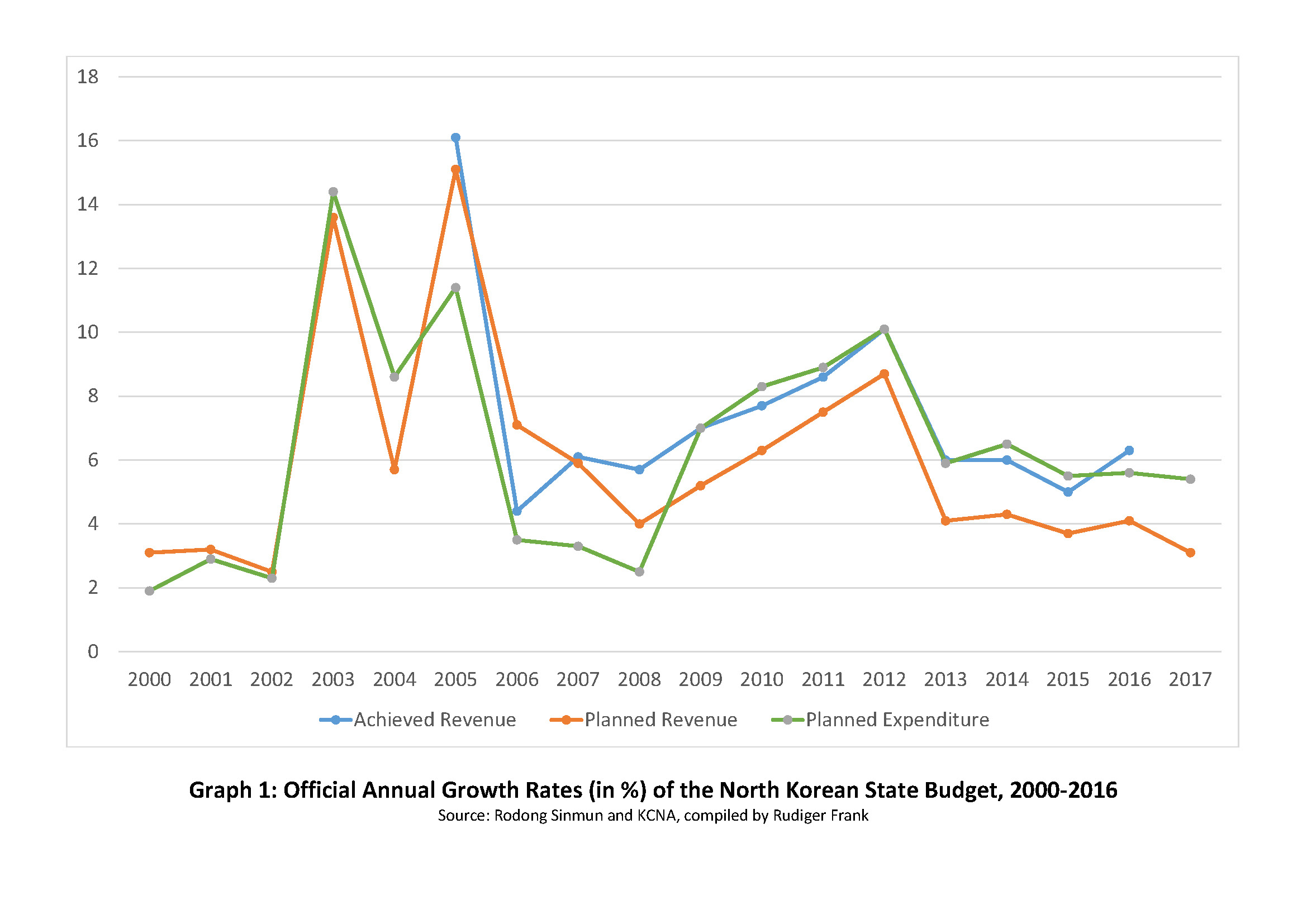

A look at the state’s data on the budget reveals a moderate but steady growth in the range of 4 to 6 percent in 2016. Considering the dominant state ownership in the North Korean economy, these numbers are at least correlated, if not equivalent to, what we would call GDP growth.

The budget reports imply that the North Korean state has for many years run a surplus, to which revenue from “local” sources—including markets—has contributed. This could help finance part of the trade deficit shown below. It is difficult to estimate the actual size of this factor since we neither have absolute budget numbers nor do we know how far the state is able to convert North Korean won into hard currency for imports. We also do not know whether the latter is necessary—for example, in case some of the state’s budgetary revenue is coming directly in the form of hard currency. Nevertheless, it is important not to see the trade reports below without some domestic context.

The KOTRA Reports on North Korean Trade in 2015 and 2016

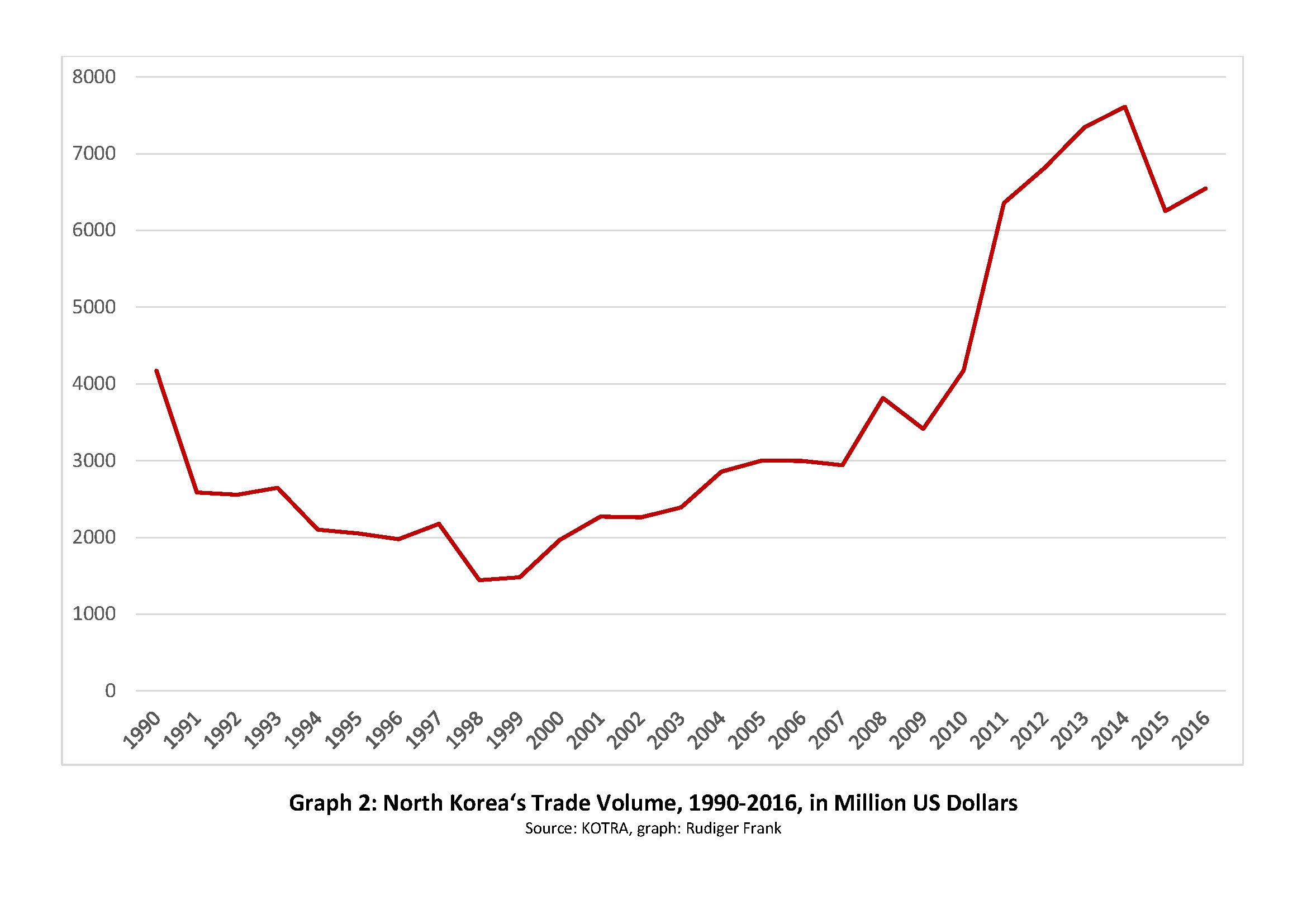

In the latter half of 2016, the South Korean Trade-Investment Promotion Agency (KOTRA) unveiled its report on North Korean trade for the year 2015. The data showed that the phase of 16 years of continuous growth of North Korea’s trade since the dramatic low in 1998 had ended. In 2015, North Korea’s overall trade volume declined from 7.61 billion to 6.25 billion USD.

Were the sanctions finally biting? But which sanctions, in 2015? UNSC resolutions 1718, 1874, 2087 and 2094 were all passed either before or during 2013, the year of the third North Korean nuclear test. But in 2014 and 2015 no tests happened, and no new UN resolutions leading to new sanctions on North Korea were passed. The reasons for the drop in North Korea’s trade volume in 2015 were rather profane. Referring to the work of Lee Jong-Kyu, Li Tingting suggests that the reasons for this decline were reduced demand by the Chinese steel industry for North Korean coal and growing environmental concerns, combined with a decline of world market prices for anthracite. Simply speaking, North Korea has witnessed the fate of any country with a trading structure that is disproportionally dependent on only one or two major export items. This example shows how careful we need to be with interpreting trade data, especially if they are strongly aggregated.

The most recent KOTRA report was released in July 2017, covering North Korea’s trade during 2016. This time, common sense would indeed tell us to expect a drop in North Korea’s trade volume. Responding to two North Korean nuclear tests in January and in September, along with a few missile launches, the UN Security Council passed Resolution 2270, further tightening its sanctions. In March, South Korea closed the Kaesong Industrial Zone which has been accused of providing over 100 million USD annually for the regime’s imports. Even China, with great fanfare, made a point of reducing its coal imports from North Korea since March 2016.

But against all expectations, the updated graph shows that the trade volume has actually recovered, although it still remains below the level of 2012. It is obviously premature to speak about a crisis or a collapse of foreign trade that would be comparable to the catastrophe of the mid-1990s. The question remains, however, how it is possible that the North Korean trade data show such a more or less continuous upward trend despite the international sanctions.

To start, we need to be aware that the KOTRA reports offer ample room for interpretation and speculation. They typically do not include inner-Korean trade. About 90 percent of the overall recorded volume is based on bilateral exchanges between North Korea and China; Boydston argues that not much else matters, especially for sanctions. Indeed, trade with other nations is so small that a single successful or failed deal, no matter how profane and non-political the reasons, can have a significant impact. In other words, most of the time, when we talk about North Korea’s foreign trade, we actually talk about trade with China.

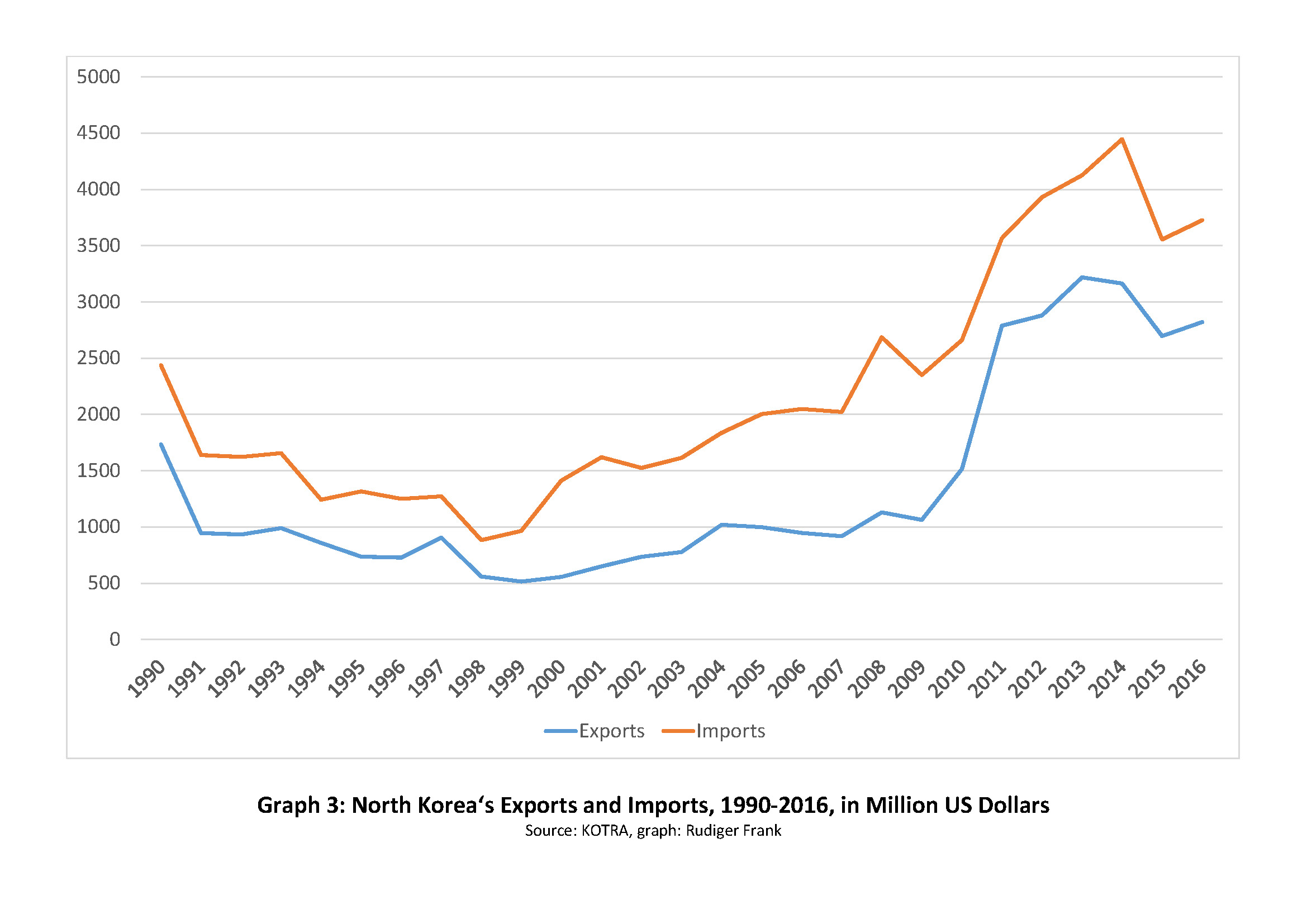

Moreover, aggregate trade data as in graph 2 hide the fact that North Korean exports had reached their peak already in 2013, and have been lower ever since. The drop after 2013 does correspond with known facts. Li (op. cit.) points at the case of Jang Song Thaek and convincingly argues that his execution in late 2013 seems to be responsible for the absence of a successful major initiative that would have made up for the reduced world market value of North Korea’s coal. The destiny of the various ill-fated Special Economic Zones in or near the Northwestern border town of Sinuiju is a case in point. They were said to be closely related to Jang and have seen little progress since his death.

On the other hand, many other bilateral trade initiatives remained intact and operating. This includes tourism, business via Dandong, the export of North Korean labor force to sunset industries such as textile factories in China, and the operation of the Rason Special Economic Zone in the Northeast. Haggard notes that the drop in global commodity prices might have affected North Korean exports, but it also made its imports cheaper, thus at least partly offsetting the loss in revenue through lower expenditures. Considering that most of North Korea’s exports are in natural resources, this could indeed explain the shrinking value.

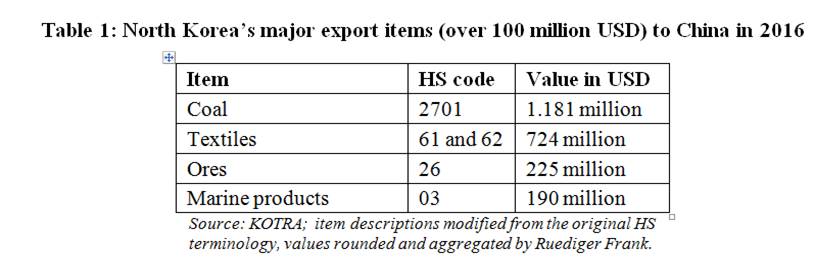

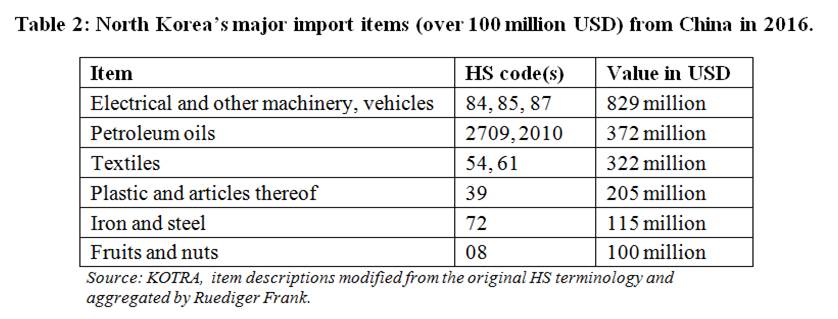

Another hypothesis—that North Korea would try to substitute sanctioned export items by other products—seems to have been confirmed, at least in principle. Noland, referring to the work of Choi and Im, argues that North Korea would try to substitute minerals with textiles. Numbers of HS 61 and 62 are indeed high, see Table 1. But this is not the whole story; substitution could also take place within the minerals section. In 2016, the exports of metals such as iron and steel have increased by over 42 percent compared to the previous year. So far, and despite this impressive growth rate, their export value (HS 72-83) stands at relatively modest 143 million USD, which is still far below the 245 million in 2013. It is thus too early to identify a real change of strategy here.

But if North Korea’s revenue through the export of coal is dropping, should this not have an impact on its imports and on its trade deficit? The logic is, again, quite simple: if you earn less money, and if nobody is giving you a loan, then you can spend less money. In fact, such considerations are behind sanctions that try to curb North Korean exports.

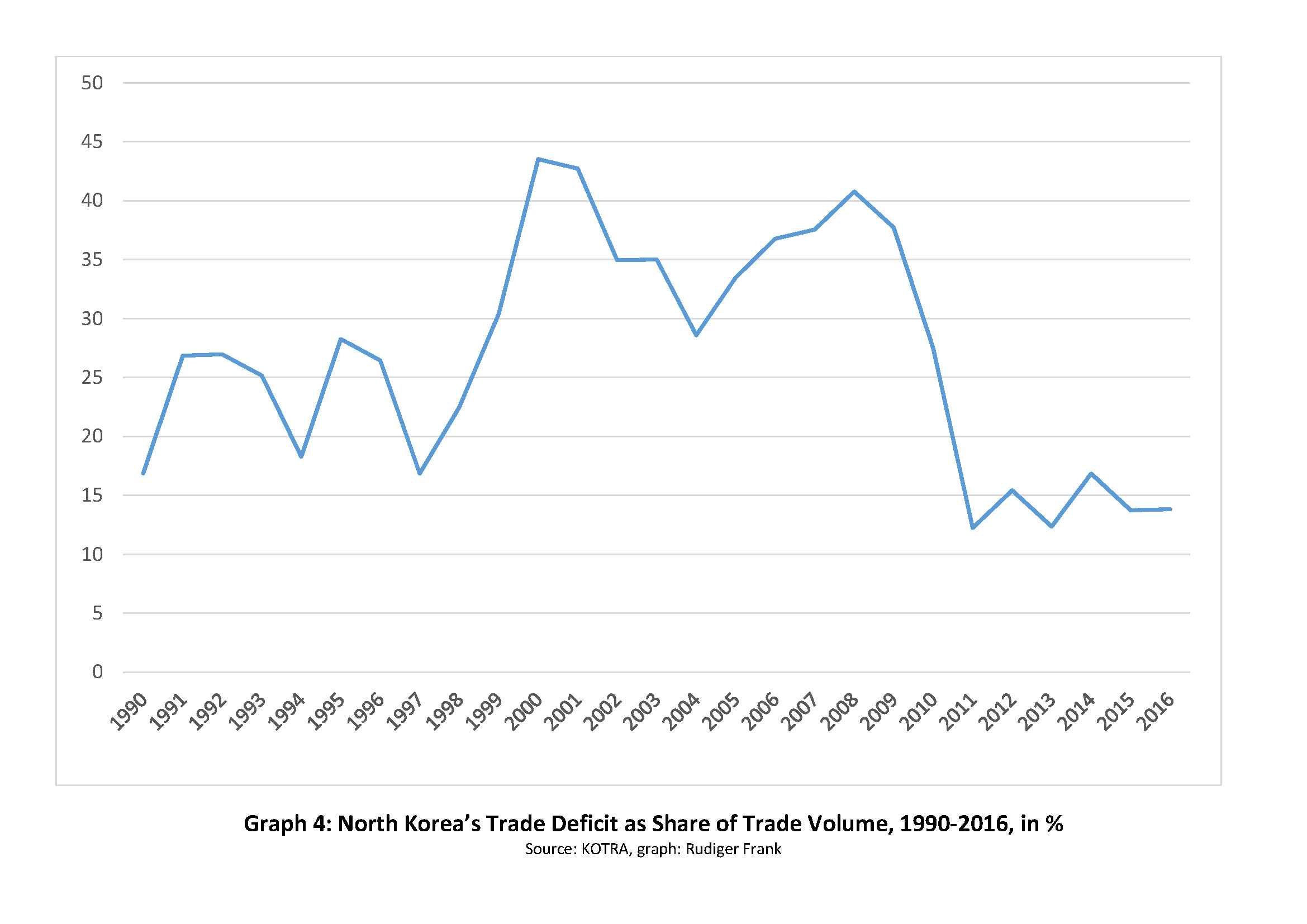

However, a look at the latest KOTRA report reveals that the North Korean trade deficit declined from 1.28 billion USD in 2014 to 0.86 billion USD in 2015 and remained at about that level at around 0.9 billion USD in 2016. It is now way below the trade deficit average of 1.1 billion USD for the years 2005-2012.

This is an interesting observation considering the closure of the Kaesong Industrial Zone in early 2016 by the South Korean side. Supporters of the measure argued that cutting off this rare source of hard currency revenue would hit the North Korean economy hard. However, the KOTRA data neither reveal a reduction in North Korean imports nor in its trade deficit. In fact, North Korean imports in 2016 increased by 170 million USD over the previous year. One source of payment for this could be the revenue generated from transfers, including remittances from workers employed abroad. Their number is in the range of 50,000 people. If their annual income is around 10,000 USD, then they earn their country 500 million USD in hard currency income. This alone would cover two-thirds of the annual trade deficit.

Considering the current debate about cutting off North Korea’s oil supply, it is interesting to note that the import value of mineral oil and oil products from China in 2016 was only less than half of such imports in 2012, when they stood at 773 million USD. Measured in tons, the amount in 2016 was 799,000 while it was 705,000 in 2012. The imported amount of oil from China has remained more or less stable, but it now costs only half as much as it did a few years ago. A hike in world market prices for oil would thus have a much more serious effect on North Korean oil imports than most sanctions.

We also find that at current prices, with cash reserves of, for example, 2 billion USD, the North Korean government could easily cover their oil imports for the next five years without exporting a single item.

Can More Sanctions Stop Kim Jong Un?

North Korea’s nuclear and missile programs are a means towards an end, not an end in and of themselves. A case in point was the announcement of the byungjin policy in 2013—of simultaneously developing the economy and nuclear weapons—which replaced the military-first policy of the Kim Jong Il era. Kim Jong Un made his order of priorities very clear: He does not just want to develop the economy so that the military would be financed properly. Rather, he repeatedly stressed that he regards a reliable nuclear deterrent as the safety guarantee that would allow him to focus on economic development. At the 7th Party Congress in May 2016, Kim pronounced, albeit in somewhat nebulous terms, a five year plan for economic development.

If the above is true, then Kim Jong Un is indeed more vulnerable to economic sanctions than his predecessors. So do more sanctions have a chance to stop the North Korean WMD program?

My answer is a plain “No.” I am not even asking whether China would ever let a collapse of North Korea happen, or whether an immediate collapse would trigger a desperate last-ditch military adventure that would result in North Korea’s annihilation but would cost hundreds of thousands of lives. A sober reality check is sufficient.

Both North Korean programs—nuclear and missile—have a history of decades. This means that critical knowledge and hardware have been acquired long before the current sanctions have been put in place. We cannot prevent them from acquiring what they already have.

Furthermore, North Korea has been pursuing self-reliance since the early 1960s even though they have actively exploited international economic cooperation from aid to trade. Nevertheless, this long-standing focus on autonomy helps explain the resilience of the North Korean national economy against measures that would have brought most other economies to their knees.

Worse even, North Korea now seems able to manufacture many if not all components of its WMD program by itself. If the North Korean military is mainly or exclusively purchasing from the North Korean state, then even the availability of hard currency is not an issue.

All this helps explain the so far low effectiveness of any sanctions, even including those that try to curb North Korea’s overall trade. Those who believe that a drastic reduction in trade will lead to an immediate change of mind in Pyongyang should consider this: Only ten years ago, North Korea was able to exist comfortably with just one third of its current trade.

The only ray of hope for supporters of total sanctions is offered by the new middle class. Their emergence is closely connected to foreign trade, which is a source of items to sell and to buy, but also a source of cash and, most importantly, domestic demand. North Koreans will only buy more, and thus provide more growth opportunities for existing or new businesses, if they have more income. My impression is that the fast growth of market activities in North Korea of the past years has recently started to slow down. Some ventures I know have already been forced out of the market due to declining sales. North Korea needs to open its economy to provide enough demand for further growth, but this requires cooperation, not sanctions.

Supporters of sanctions could hope that a disgruntled middle class would therefore pressure its government to give in to Western demands so that they regain their opportunities for growth and profit. The problem with this reasoning is that it assumes North Koreans are only driven by greed, and that the state has no means to put the genie back in the bottle. Both are true, but only to some extent: let’s not forget the massive repression apparatus. But more importantly, North Koreans are nationalists. If their government can make them believe that the country is really on the brink of a war, then they will postpone their desire for profit and rally ‘round the flag and the leader. The late Don Oberdorfer called this phenomenon “siege mentality.” Admittedly, North Koreans are used to a high dose of tension and bellicose rhetoric, but the utterances of Donald Trump (“fire and fury”) and people around him, like Nikki Haley (Kim is “begging for war”) constitute a new level of verbal threat. Combine this with the annual joint US-ROK military maneuvers, the stationing of THAAD in Seongju and China’s open criticism to it, Japan’s push for remilitarization, and new UNSC Resolutions and sanctions, and you might see exactly what Kim Jong Un needs to keep his system stable.