The North Korean Economy in April 2019: Sanctions Are Pinching—But Where and How Much?

Wonsan-Kalma and the North Korean Economy

What does one single resort construction project on North Korea’s east coast say about the state of the country’s economy?[1] Quite a bit, perhaps: it’s not just North Korea’s low exports that are causing problems. A bigger issue is importing goods for industrial production and construction. Kim Jong Un claimed as recently as last week that he isn’t “desperate” for sanctions relief. That may be true. After all, the North Korean regime’s threshold for economic pain is quite high. But looking at the data, there is no denying that sanctions are hurting North Korea. The only question is how much.

In early April, Kim Jong Un visited the Wonsan-Kalma Coastal Tourist Area construction site. According to an April 6 report in North Korea’s Korean Central News Agency (KCNA), Kim decided to extend the construction deadline by over a year to April 15, 2020, the day of Kim Il Sung’s birthday. Rather than “push forward the construction of the Wonsan-Kalma coastal tourist area in a hurried way to finish till the Party founding anniversary this year,” Kim said that postponing would be better, so that workers could “perfectly finish it.”

On the one hand, this could be seen as a pragmatic act. Stories abound of workers pushing ahead to finish a specific construction deadline for political reasons, particularly in socialist countries. Kim emphasized that the construction “should never be carried out in a slipshod manner, stressing the speed only,”—quite a different tone from that of state propagandists during North Korea’s shock-work Chollima campaign in the 1950s and 1960s. Perhaps the apartment building collapse in Pyongyang in mid-May of 2014 left a lasting legacy, and caused authorities to put a higher priority on safety in construction projects.

On the other hand, this is the second time that Wonsan-Kalma’s project deadline has been extended. The state of construction is a microcosm for the impact of sanctions on North Korea. Rather than having a broad impact on the country’s economy as a whole, sanctions are hitting North Korea in specific ways that are not always easily noticeable to the outside world. That does not make them any less real.

We often look at the state of North Korean exports as a measure of how sanctions are hitting the country. As seasoned North Korea expert Bill Brown often points out, for an economy like North Korea’s, fluctuations in exports only really matter to the extent that they either allow or constrain North Korea’s ability to import. For North Korea, maintaining a stabile trade balance is not intrinsically important. But it needs to export in order to be able to import.

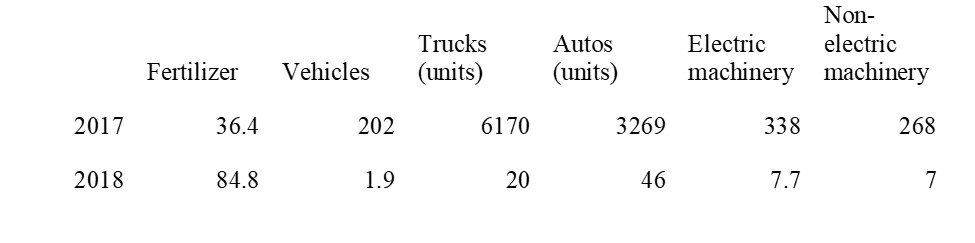

This is particularly pertinent for domestic industry. Spare parts and the like are needed for any country’s industrial base to function smoothly. The same goes for construction. Looking at the balance sheet for North Korea’s imports from China in 2018, several categories of goods used in industries such as construction have plummeted.

North Korean Imports from China 2017-2018

We don’t know if these imports have dropped so steeply because of the judicial obstacles that sanctions create, or because North Korea doesn’t have the money to pay for them. At the end of the day, however, it doesn’t really matter that much. Of far more importance, is that it is likely the country’s industries, including construction, are significantly constrained by the sanctions and geopolitical situation. To say that sanctions are rendered “ineffective” by smuggling, as the most recent UN Panel of Experts report did, is a massive exaggeration. Smuggling can only make up for a relatively modest proportion of what North Korea loses through a fall in trade, both exports and imports; smuggling also imposes a high risk premium, both in what North Korea gets paid for its smuggled exports and in what it has to pay for clandestine imports. Whether this affected Wonsan-Kalma specifically is impossible to say with certainty, but it may well be the case.

The Harvest and Food Shortages

Not all negative developments in the country’s economy, however, are attributable to sanctions. The food situation appears to be increasingly difficult, but the sanctions regime has not likely been a major factor. North Korean imports from China of some food products and fertilizer increased in 2018 compared to the prior year. Fertilizer imports, for example, shot up by about 133 percent. None of these goods are covered by the sanctions regime. Gasoline prices in the country have been permanently higher since sanctions were put in place to cap North Korea’s fuel imports. The general decrease in fuel supply may have affected agricultural production, since fuel for transportation of production inputs and agricultural machinery is more expensive. But there could have been, in theory, countervailing effects as well, that make the production of some goods comparatively cheaper. Fertilizer production in North Korea, for example, is primarily based on coal, since the country shifted its fertilizer plants to use coal instead of petroleum some years ago.[2]

The main cause of the declining harvest appears to be inclement weather through the spring and summer of 2018 and North Korea does not have a resilient agricultural economy to cushion such shocks. Whatever agricultural reforms and institutional changes Kim Jong Un has actually instituted, we know very little still about the extent of their implementation. But it does seem that whatever systemic changes Kim has made, they have not yet had a significant impact on agricultural production.

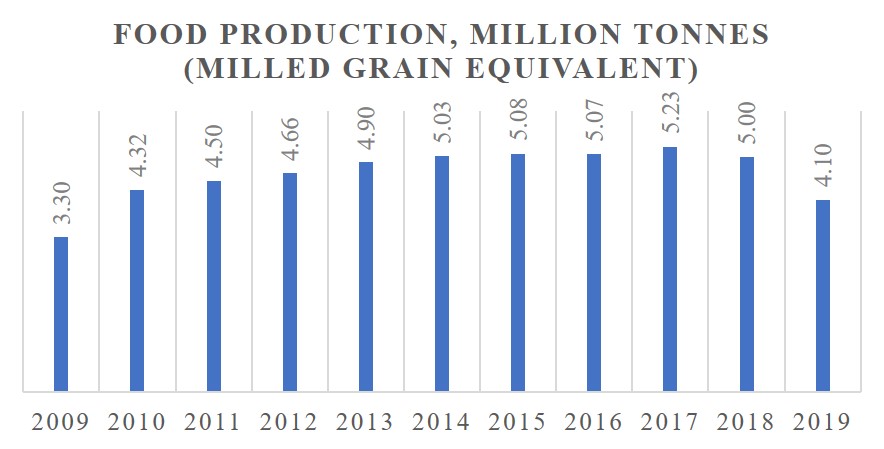

So how large was the harvest, and how should we understand it in context? Judging by the numbers, the situation looks significantly worse than it has in the past several years. It doesn’t appear disastrous; however, when many North Koreans are already getting by on very little, a lower harvest may have dire consequences for a significant proportion of the population.

There are several ways to look at these numbers. The graph below presents my own estimate of the milled cereal equivalent of the food production figure given by the World Food Program/Food and Agricultural organization (WFP/FAO).[3]

By this measurement, the production drop appears significant—around 18 percent from 2018. There are other ways, of course, to measure total food availability in the country. Nonetheless, this rough order of magnitude measurement shows that 2018 food production is the lowest harvest figure since 2009, when harvest figures began to climb significantly.

One of the key questions is the extent to which the general public still relies on public distribution of food. By almost all accounts, the general public distribution system has been disbanded for the past few years. Specific professional groups still get food distribution, however, from the state through their places of work. Daily NK reported last month, for example, that in some state organs, employees were receiving only 60 percent of what they usually get in food rations.

Market prices have remained stable through the winter and early spring, both for rice and foreign currency. The latest price observation by Daily NK does not indicate that anything is out of the ordinary—as of March 26, rice prices continue to hover around 4,000 won/kg, and market exchange rates for US dollars and Chinese renminbi remain around their normal levels (roughly 8,000 and 1,200 won respectively).

However, none of this means we can simply conclude that North Korea’s food situation is stable. At face value, things may look fine because food prices haven’t shifted much after news of the relatively poor harvest came out. But generally, food prices tend to spike only in the early fall months, prior to the coming year’s harvest. That’s likely when shortages first become truly visible and tangible for market actors. Even with this year’s poor harvest, it’s possible that market actors simply don’t have enough of a macro-level understanding of the food supply outlook for prices to climb at this time.

Moreover, it is uncertain how much the general public relies on the markets rather than state distribution for sustenance. Some defector surveys suggest that people rely on the markets for about 70 percent of their food provision. These surveys, however, tend to be extremely skewed toward the border regions, and defectors are involved in market- and cross-border trade to an unrepresentatively high degree. One 2017 survey, for example, was based on a sample where 88.6 percent of those surveyed were from North Hamgyong and Yanggang provinces.[4]

It’s also possible that prices aren’t rising because they already are at the highest level that consumers can afford. Put simply, if people don’t have enough money to spend on food at a higher price, it would make little sense for suppliers to raise their prices. Economists call this the “reservation price” of consumers—the highest price that buyers in a market are willing to pay for a good. Anecdotal reports suggest that large numbers of North Korean workers have lost their jobs following factory closures resulting from sanctions. If consumers have less disposable income to spend on a product, it might not matter if supply is shrinking: prices must remain at a level where consumers can afford them.

A sharp rise in food prices would indicate a truly disastrous food situation. That said, a shortage can still be very dire and problematic without throwing the country into famine. Simply put, absence of dramatic price shocks should not be conflated with a stable food supply.

Conclusion

The construction delay at Wonsan-Kalma is a potential symbol of how much sanctions are hurting North Korea’s economy: the country is not in a disastrous pinch because of sanctions, but it is very much feeling the pain. Many industries, including construction, are likely facing stark shortages of spare parts and other equipment.

Although this year’s harvest doesn’t seem disastrous compared to previous years, the numbers do give cause for concern. The country’s food situation is difficult to survey comprehensively because the government doesn’t allow international organizations access to the markets; even so, a lower harvest may well lead to more serious shortages on the markets as the fall season approaches, when market prices typically climb.

- [1]

This is the first in a column series on issues in the North Korean Economy, to appear monthly on 38 North. This column is partially based on a discussion between the author, Bill Brown, and Randall Spadoni, and the author is grateful for their valuable insights. Opinions and errors belong solely to the author.

- [2]

I am grateful to Bill Brown for pointing this out.

- [3]

“Milled cereal equivalent” refers to a measurement of food production that essentially turns agricultural products of varying nutritional content into one, unitary equivalent measurement. (For more on this, see this 38 North piece by the late scholar Randall Ireson.)

- [4]

This is a methodological difficulty that is virtually impossible to overcome under present conditions, and none of this should be taken as a criticism of the survey itself. It is up to us as readers and users of this data to continuously contextualize it, recognizing the limits of the sample it rests on.