“Maximum pressure” and the North Korean economy: what do market prices say?

By Benjamin Katzeff Silberstein

With the news today about a summit between Kim Jong-un and Donald Trump tentatively planned for the end of May, there has been much debate about the role of the US policy of “maximum pressure” through economic sanctions.

The efficacy of the policy is difficult to evaluate, particularly since it often takes many months or even years for the full effect of sanctions to play out. Whether the policy has been effective or not depends on, well, how you judge success or failure. There is little doubt that North Korea’s exports have taken a significant hit not primarily from the sanctions themselves, but from China’s enforcement of them. This is the single biggest difference between how sanctions have hit the North Korean economy during the past year, versus previous years. It seems fairly indisputable that sectors of the economy have suffered, with export industries taking the biggest hit.

But what has been the impact on the economy as a whole? It’s difficult to say, but we have two important indicators: prices of rice and foreign currency on North Korean markets. The data on these two indicators is far from perfect, and it is difficult, if not impossible, to draw firm conclusions from it. (For an explanation of this data, and the rationale for using rice prices in lieu of the formal goods basket used to measure inflation in other countries, see this article, for example). Nevertheless, neither of the two indicators suggest a situation out of the ordinary on North Korean markets during the period that “maximum pressure” has been applied.

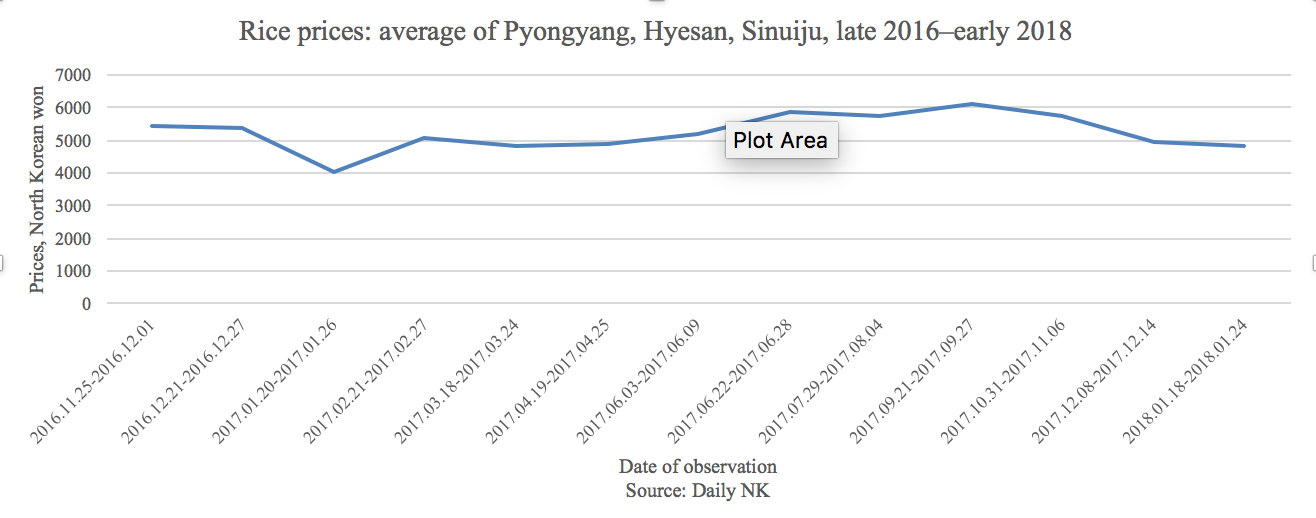

First, a look at rice prices. If sanctions were truly devastating the North Korean economy, there is a whole host of reasons why one should expect rice prices to increase.

One of them is expectations of worse times to come as importing inputs for agriculture as well as food becomes increasingly difficult. Another is that if importing food products in general* becomes more difficult, perhaps because Chinese traders anticipate that their North Korean counterparts won’t be able to pay, consumers would be expected to switch more of their consumption to domestically sourced goods, increasing demand and thus prices. In general, anxiety about worsening times often leads to inflation.

This does not seem to have happened. In fact, rice prices have been remarkably stable over the past year (if the graph looks strange, click for full image):

There may well be other forces at work, too. Increased smuggling of cheaper Chinese rice, for example, may well have contributed to the price stability. But this is in itself a sign of the resiliency of the North Korean economy; when some supply decreases, there are ways of compensating through other means.

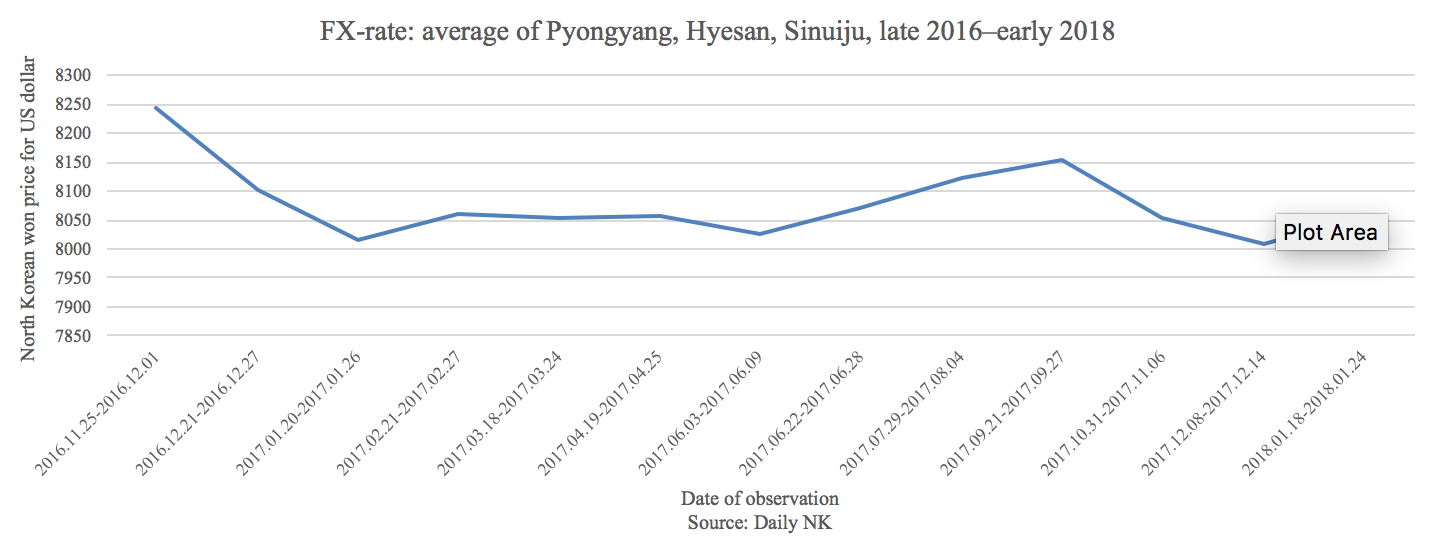

Exchange rates are another important metric. If the inflow of foreign currency (in this case US dollars) decreases, its price – the exchange rate – should go up. Expectations matter here, too: if the market expects that foreign currency supply will dry up in the future, it tends to act in the present and make purchases today to hedge for tomorrow. As with rice prices, exchange rates have been remarkably stable over the past year (again, click for better image):

In sum, we have little or no hard evidence that the North Korean economy, on the whole, has suffered significantly and harshly from sanctions thus far. That may itself not be an argument against sanctions, since again, it may take much longer than just a year for their full impact to play out. But it does call into question the claims that “maximum pressure” is the chief reason for Kim Jong-un’s outreach to Donald Trump.

*This likely holds true regardless of the level of self-sufficiency in North Korea’s agricultural production.

View Original Article