North Korea’s Economy, H1 2026: A Sliding Won and a Tungsten Windfall

This article is from the fifth edition (April–June 2026) of 38 North’s quarterly product, North Korea Briefing, that monitors key internal developments in North Korea. For the full series, click here.

Two developments defined the North Korean economy in the first half of 2026. The first was monetary: the won fell steeply and market prices surged alongside it. The second was a windfall in mineral exports, driven by global, particularly Chinese, demand for tungsten rather than Pyongyang’s own doing. Together they reveal a single condition: North Korea can still earn meaningful foreign exchange when global prices move in its favor, even as it loses its grip on its own currency at home. The windfall rested on a volatile price the state neither set nor controlled, while the currency instability was largely homegrown—meaning the external gains did little to stabilize the economy, and the two developments are best understood as largely independent.

A Sliding Won and Monetary Inflation

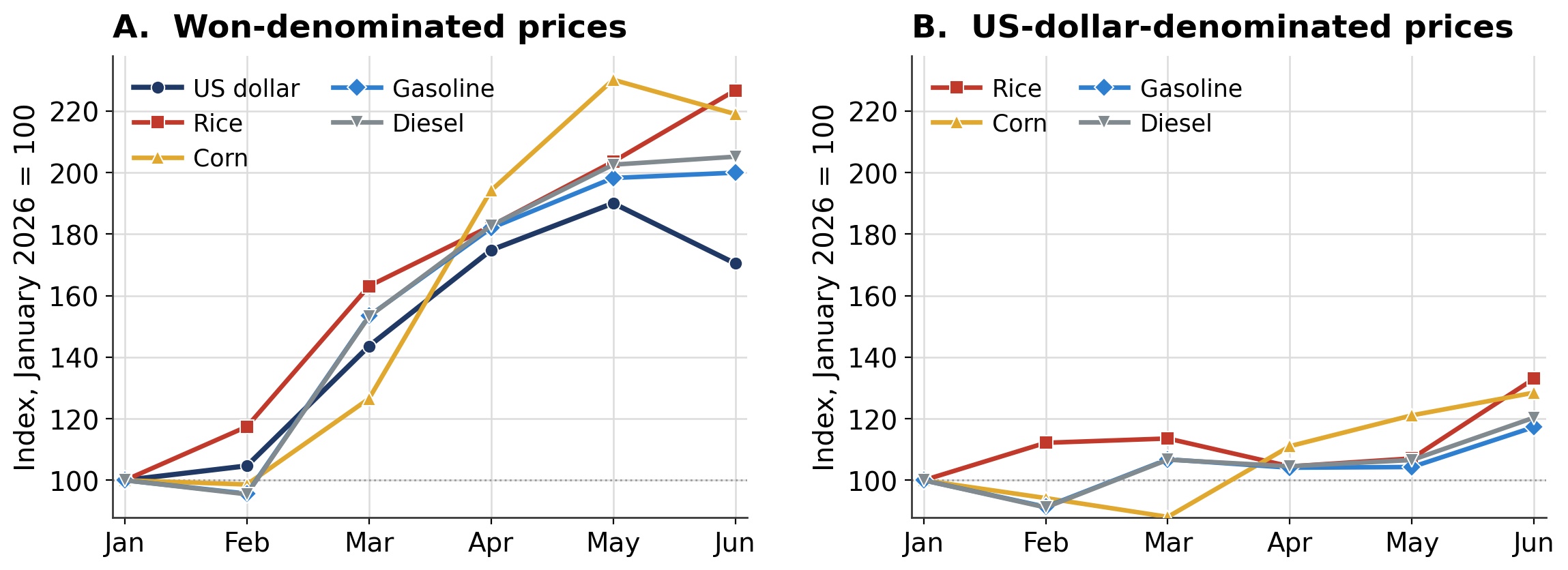

The clearest signal of the first half came from the won, whose market exchange rate fell steeply against the US dollar and the Chinese yuan as prices in won terms rose: the dollar climbed to a May peak about 90 percent above its January level—from roughly 37,250 to 70,800 won—before easing in June, while won prices for rice, corn, gasoline, and diesel roughly doubled (Table 1).[1] The acute depreciation ran from March to May, with the won partly retracing in June. Even granting that private markets may have receded since the pandemic era recentralization, making retail prices a narrower gauge, the move read as an economy-wide monetary event, not a market-specific one. It runs through the exchange rate on which the country’s heavily dollarized transactions are based. Over a longer horizon, the scale is considerable: the dollar’s won price has risen roughly seven-and-a-half-fold since early 2024, with the won shedding most of its external value in barely two years.

The decisive evidence that depreciation, not scarcity, drove the surge comes from repricing these goods in hard currency. Through June, dollar prices rose only modestly—rice from $0.41 to $0.55 per kilogram, fuel from $1.03 to $1.27, and corn from $0.10 to $0.13—even as won prices doubled (Figure 1, Panel B); fuel, which has no spring lean season effect, moved in near-lockstep with grain. Prices rose because each won bought steadily less foreign exchange; in the North’s dollarized markets they are set effectively against the dollar.

The distributional consequence follows directly. With dollar prices broadly stable, those who earn or hold hard currency—traders and the donju entrepreneurial class—saw their real purchasing power largely preserved through June. The burden fell on the won-dependent: state enterprise wage earners and others paid in won, whose nominal incomes do not adjust with the exchange rate. For them, a doubling of food and fuel prices in won within months is a sharp, regressive real-income shock that any aggregate inflation figure would understate. These strains are visible in market behavior, with an accelerating flight from the won and a coercive state response.[2]

Context and Implications

Why the won is falling is harder to establish. A move this large—a near-doubling in months—is far larger than any plausible trade balance swing could produce, and there is no sign foreign exchange earnings were contracting. If anything, overseas labor and mineral receipts were rising, with labor earnings in particular bolstered by the continued dispatch of workers to Russia amid the war in Ukraine.[3] That points away from a foreign exchange shortage toward domestic causes, of which two fit the evidence and are not mutually exclusive.

The first is monetary. Excess won liquidity, beyond what hard currency supply can back, would depreciate the won fairly mechanically. Two channels plausibly drove it: financing the regime’s construction and regional development commitments, and the campaign of state wage and price increases North Korea has pursued since late 2023 to revive its planned economy and state commerce. A cabinet resolution lifted nominal public sector wages roughly tenfold—reportedly up to 40 or 50 times in priority sectors—alongside parallel hikes in state-set prices.[4] Paying out far more nominal won without matching output is monetary expansion. Observers tie this directly to rising prices, and broad, roughly proportional co-movement of prices and the exchange rate is its signature. On this reading, the campaign is itself a deliberate repricing of the state sector, and the won’s slide may be a tolerated—even intended—outcome rather than an unwanted side effect; the data cannot settle intent, since the evidence fits an undesired byproduct of monetary financing equally well.

The second cause is expectational. A loss of confidence in the won, potentially self-reinforcing once depreciation begins, can drive households and traders out of won and into dollars and yuan irrespective of fundamentals. The public’s distrust has deep roots, going back to the 2009 currency redenomination, and mass wage increases financed by money creation, along with the state’s crackdowns and warnings in response to the won’s steep fall, have only driven further flight from the local currency.[5]

A Tungsten Windfall: Price, Not Effort

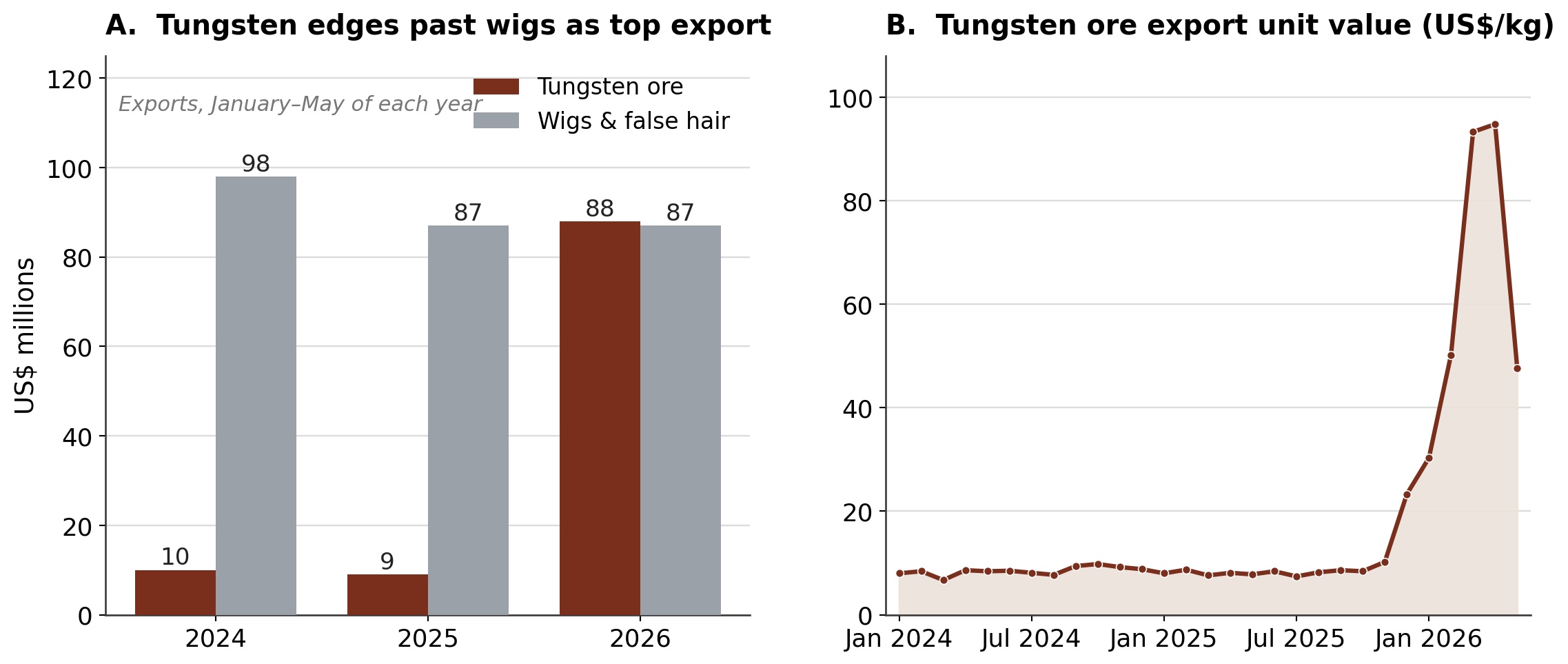

The first half’s other notable development was external and largely unrelated to the won’s slide: a surge in mineral export earnings. Exports to China rose 68 percent year-on-year over January-May, to $287 million, with roughly two-thirds of that increase from a single export line: tungsten ore, whose value leapt nearly tenfold, from about $9 million a year earlier to $88 million (Table 2).

The windfall was almost purely a price phenomenon. Shipment tonnage rose only about 15 percent; the average unit value jumped from around $8 to nearly $70 per kilogram—some 98 percent of the earnings growth (Figure 2). The unit price proved volatile: the monthly unit value spiked above $90 per kilogram in March and April before halving to around $48 in May. The cause lies entirely outside North Korea: China, which controls more than three-quarters of global tungsten supply, placed tungsten products under export licensing in February 2025 and tightened controls through 2026; benchmark prices for ammonium paratungstate rose about 218 percent over 2025 and reached record highs in early 2026.[6] As a marginal supplier to Chinese processors, North Korea received far more for roughly the same volume.

Context and Implications

The shift has reshaped the country’s export profile. Mineral ores, barely a tenth of sales to China a year earlier, now make up about a third. For years the North’s largest export had been wigs and false hair—the labor-intensive output of its processing-on-commission trade—but over January-May 2026 tungsten drew level and narrowly edged ahead for the first time. The change marks a move from an export reflecting North Korean labor to one reflecting a price the country neither sets nor controls. The earnings are real, but they represent a windfall hostage to a volatile global market, as the May price pullback illustrates, rather than evidence of durable productive capacity.

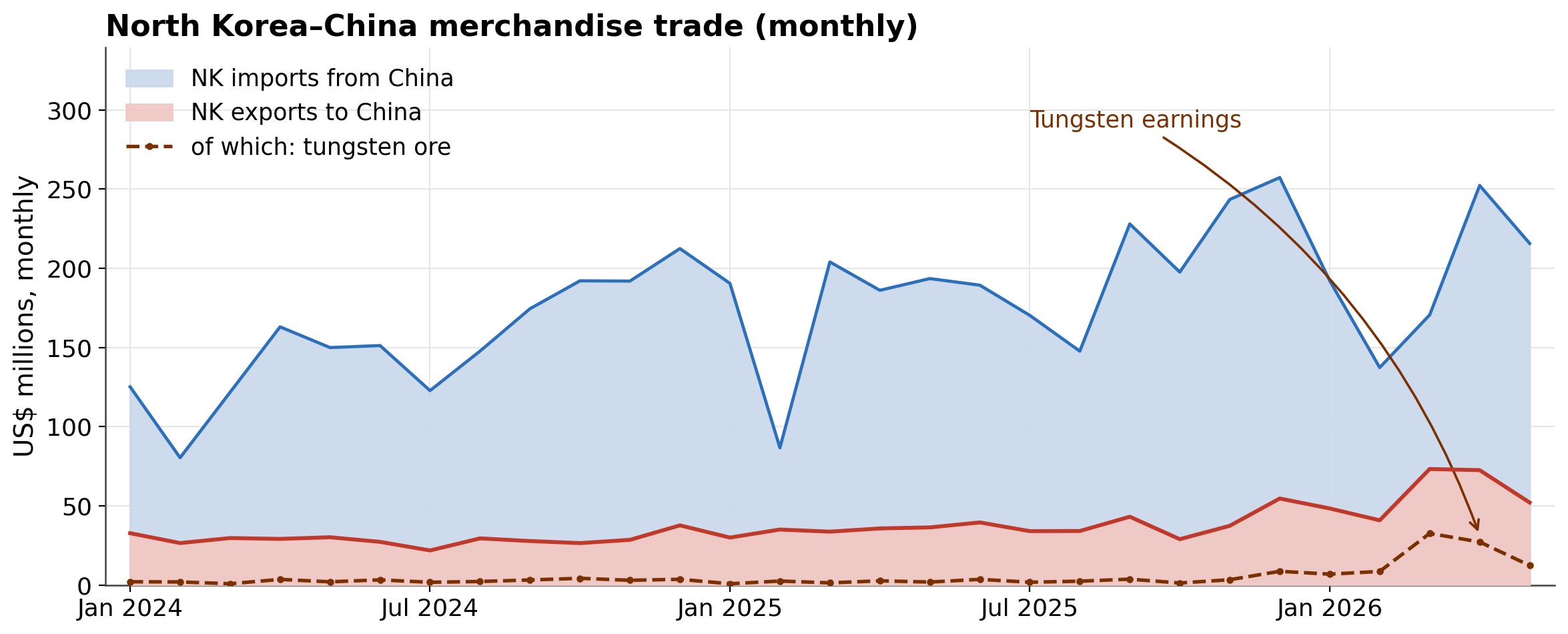

Substantial as it was, the windfall does little to alter North Korea’s external accounts (Figure 3). At roughly $16 million a month in extra earnings, it is dwarfed by a $194 million monthly import bill; the merchandise deficit with China was essentially flat year-on-year. The half-year’s two stories are thus independent: the tungsten boom was far too small to move the foreign exchange market, so it neither caused the won’s slide nor cushioned it.

Outlook

Both stories carry forward on separate tracks. President Xi Jinping’s June 8-9 state visit to Pyongyang—his first since 2019 and his first overseas trip of 2026—signaled a deliberate warming as Beijing moves to reassert its influence amid deepening North Korea-Russia ties and prospects for eventual US-North Korea talks. To the extent the visit leads to expanded trade, energy, or other support, it is one of the few forces that could meaningfully expand the North’s foreign exchange inflows and ease pressure on the won—though any such effect is a story for the second half, and past Chinese support has rarely been transformative.

June’s partial rebound in the won is welcome but too short-lived to be relied upon; its path will hinge less on the autumn harvest than on how much liquidity the authorities continue to inject to finance priority projects. The tungsten windfall will rise and fall with a market set in Beijing and beyond—lucrative while it lasts, but no foundation for a recovery.

- [1]

Figures throughout use market (informal) exchange rates, where most transactions occur. North Korea’s official rate is set far stronger—about 100 won per dollar, according to Daily NK, severely overvaluing the won. Most North Koreans neither use nor know this rate. State-run exchanges instead posted a fixed rate of roughly 8,900 won per dollar for much of 2024, before being adjusted toward the market rate in 2025. See Seulkee Jang, “N. Korea narrows gap between official and market exchange rates,” Daily NK, April 3, 2025, https://www.dailynk.com/english/n-korea-narrows-gap-between-official-and-market-exchange-rates/.

- [2]

Dollars are increasingly used for everyday transactions, even by Russian visitors at the new Wonsan-Kalma resort, while currency hoarding and doubled transport fees fed into higher prices and thinner consumption. The state has responded by banning private foreign-currency trading, cracking down on money changers, injecting emergency cash to steady fuel prices, and blaming the exchange-rate rise on “unfounded rumors.” See William Brown, “Power on Parade but Crisis at Home as North Korea’s Economy Wavers,” Korea Economic Institute of America, October 8, 2025, https://keia.org/analysis/power-on-parade-but-crisis-at-home-as-north-koreas-economy-wavers/; Benjamin Katzeff Silberstein, “What’s Up with North Korea’s Skyrocketing Exchange Rates?,” 38 North, October 2, 2024, https://www.38north.org/2024/10/whats-up-with-north-koreas-skyrocketing-exchange-rates/.

- [3]

On the scale and direction of North Korea’s overseas labor, including the continued dispatch of workers to Russia, see Global Rights Compliance, “New Report Reveals Testimonies of North Koreans Exploited Across Russia in 100,000-Strong Global State-Sponsored Forced-Labour Programme,” March 2026, https://globalrightscompliance.org/new-report-reveals-testimonies-of-north-koreans-exploited-across-russia-in-100000-strong-global-state-sponsored-forced-labour-programme/. The UN Panel of Experts estimates the overseas labor program generates approximately $500 million a year; rising mineral receipts are documented in the China customs data discussed below (Table 2).

- [4]

Sung Hui Moon and Jieun Kim, “North Korea boosts salaries, introduces cash cards for more currency control,” Radio Free Asia, January 17, 2024, https://www.rfa.org/english/news/korea/cards-01172024143010.html; Seulkee Jang, “N. Korea raises wages tenfold after 21 years, but companies struggle to sustain payments,” Daily NK, March 7, 2025, https://www.dailynk.com/english/north-korea-raises-tenfold-after-21-years-companies-struggle-sustain-payments/; Seulkee Jang, “Wage hikes widen N. Korean income gap 18 months after reform,” Daily NK, April 9, 2025, https://www.dailynk.com/english/wage-hikes-widen-n-korean-income-gap-18-months-after-reform/; Andrei Lankov, “How North Korea has clawed back control over the economy by hiking state wages,” NK News, May 14, 2025, https://www.nknews.org/2025/05/how-north-korea-has-clawed-back-control-over-the-economy-by-hiking-state-wages/. According to these reports, an October 2023 cabinet resolution reportedly raised state wages by roughly tenfold on average and as much as fiftyfold in priority sectors, while raising state-set prices in parallel as part of a broader effort to revive the state economy.

- [5]

On the enduring distrust created by the 2009 currency redenomination, see John S. Park, “North Korea’s Currency Redenomination: A Tipping Point?” United States Institute of Peace, December 3, 2009. On the resulting flight to hard currency and the counterproductive effects of crackdowns, see Benjamin Katzeff Silberstein, “What’s Up with North Korea’s Skyrocketing Exchange Rates?” 38 North, October 2, 2024, https://www.38north.org/2024/10/whats-up-with-north-koreas-skyrocketing-exchange-rates/.

- [6]

Shalina Cao, “Chinese tungsten product prices surge over 200% in 2025 amid export controls, fresh demand,” Fastmarkets, January 15, 2026, https://www.fastmarkets.com/insights/chinese-tungsten-product-prices-surge-2025-export-controls-fresh-demand/.