The Logistics of Funding North Korean E-Wallets

Smartphone-based e-payment systems appear to be growing quickly in Pyongyang. Several competing payment platforms in conjunction with recent accounts from visitors to the capital suggest the QR code-based platforms are widely used and accepted, from department stores down to street vendors.

Information about the spread of e-payment platforms outside of the capital is much more limited, but data obtained by NK TechLab indicates there is a push to take the networks nationwide.

The data covers lists the locations where people can deposit money into Samhung e-wallet accounts betwee 2022 and 2025. Samhung operates one of the largest smartphone-based payment networks in the country and since 2022, the network has more than tripled in size. Growth was initially centered on Pyongyang but now appears to be focused on the provinces.

Expanding use of electronic payments, which can be done in both local and foreign currencies, gives the state more insight into the domestic economy, and helps it both regulate prices and collect taxes. It can also be used as a form of surveillance, although the primary incentive is likely the economic benefits.

Background

Electronic payment services began in North Korea around 2011 when the Foreign Trade Bank issued the Narae (나래) debit card. The Central Bank followed in 2015 with the Jonsong (전성) Card, but accounts suggest both were relatively unpopular due to distrust of banks.

Citizens began using cellphones to make micropayments in the late 2010s by exchanging cellular airtime credits in lieu of money. This ad-hoc and unregulated payment system was closed by the state in 2019.

The Electronic Payment Law (전자결제법) of 2021 allowed non-banking entities, such as IT companies, to offer payment services under supervision of the Central Bank and this appears to have been the trigger for many of the platforms. At least seven competing platforms have been observed: Samhung (삼흥), Manmulsang (만물상), Huinnun (흰눈), Jonsong, Narae, Saebyol (새별) and Apnal (앞날).

Video from visitors to North Korea shows QR codes are increasingly present at many points of sale. In the case of a street food vendor or market stand, it might be a single code for a single platform, but at larger stores multiple platforms accepted.

Deposit Network

The e-wallet systems are backed by a network of locations where users can deposit cash into their accounts. In late 2022, there were around 200 such locations in the Samhung network, but by early 2025, the number had risen to over 700.

The vast majority of these locations are in Pyongyang. The city had 149 deposit points in late 2022, rising to 576 in early 2025. In the rest of the country, the number of locations jumped from 74 to 133. Most of the expansion in Pyongyang came between 2022 and 2024, while the pace of growth outside of Pyongyang picked up in 2024.

Perhaps more striking than the number of locations has been the geographic spread. In Pyongyang, there are multiple deposit locations in each district but outside of the city, the network is less concentrated. For the most part, the network has grown to include at least one location in every county. While one location per county might not meet actual demand, it has meant a rapid expansion in areas covered from 2024 to 2025 and suggests adoption of these technologies is, indeed, growing.

That said, some of the locations that existed in the 2022 data do not exist in the 2025 data. It is unclear if this is due to the service being removed or incomplete data.

Notably, the 2025 dataset lists a deposit point in every county of North Hwanghae and Ryanggang province and all districts of Nampho City, in addition to the comprehensive coverage of Pyongyang. Based on the 2025 dataset, several provinces are lagging in adoption including North Hamgyong, where only Chongjin appears to be covered.

More than half of the locations are IT Exchanges (정보기술교류실), which are physical locations where North Koreans can get help with their phone and download new apps and content.

These service centers are not run by Samhung, so they likely handle deposit services for other e-payment apps too. This theory is supported by a poster for the Huinnun e-wallet that mentions IT service centers as deposit locations.

Only a handful of the charge points are banks or post offices, which points to the root of Samhung and most other e-payment apps being in North Korea’s technology sector rather than the banking sector.

Two of North Korea’s banks, the Central Bank and the Foreign Trade Bank, operate their own cash cards. The cards, Jonsong and Narae, respectively, have companion e-payment apps but comparable data for their deposit networks is not available.

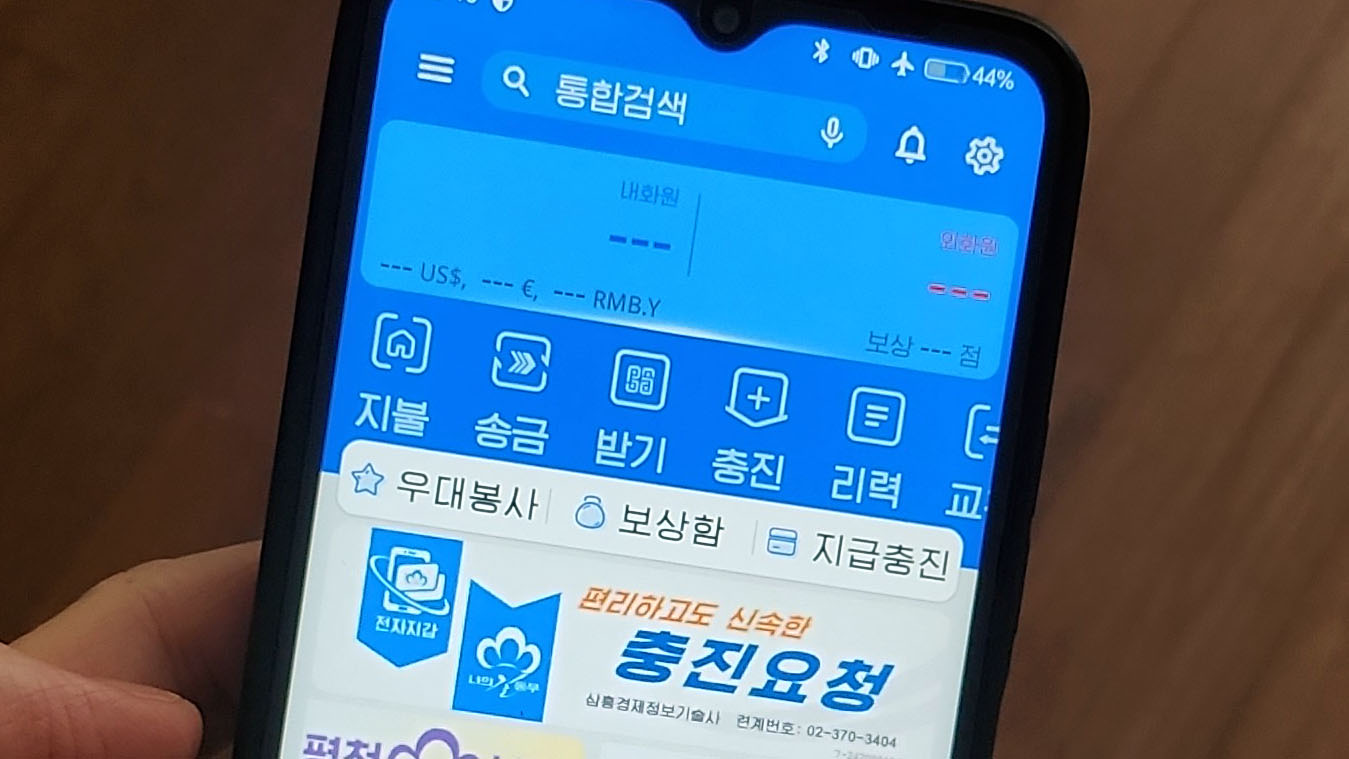

Dollars Accepted Here

One of the most interesting aspects of the e-payment platforms is that they allow users to hold more than just North Korean won. The cash is converted to foreign exchange (FX) won (외화원), a virtual currency that is used to represent foreign currencies and is worth about 110 FX won to the US dollar.

Historically, the US dollar has bought approximately 8,000 North Korean won, although this rate has substantially changed in recent years and is now around 63,000 won to the dollar.

However, the FX won and conventional North Korean won (내화원) are not interchangeable and goods are priced in one or the other. The FX won rate is set by the state and appears to be a lot more stable.

Of the locations in the 2022 dataset, all accept domestic won deposits, and the majority also accept foreign currency. In 2023, a handful of deposit points appeared to accept only foreign currency. As of early 2025, this had grown to 102 locations that only accept foreign currency deposits. All are ATMs.

Of the other locations, 341 accept only North Korean won, and the remaining 266 locations accept both foreign and domestic currency deposits.

The widespread ability to deposit foreign currency illustrates the state’s effort to capture foreign currency cash circulating in the economy. When users pay it into electronic accounts, the hard cash becomes available to the state for its use while the user gets an electronic credit that can be used to purchase goods at a later date.

ATM Networks

ATM networks also appear to be spreading alongside the growth of e-payment services. Hwawon ATMs, run by Hwawon Electronic Bank (화원전자은행), were in 15 locations in late 2024, but a more recent pamphlet advertising the network posted on Chinese social media indicates they are now in at least 40 locations. Many are in Pyongyang but the pamphlet notes: “ATMs are being introduced not only in Pyongyang but also nationwide.”

Two other ATMs have also appeared in tourist videos. One carries the Narae name and another the Taesong Bank (대성은행) name. They appear to have similar or identical interfaces. Like most North Korean ATMs, they have a card slot, 2D barcode scanner, receipt printer and keypad.

The screens of all three ATMs advertise the ability to use the machines to fund electronic wallets.

Conclusion

The data provide further evidence that the state is pushing the development and use of electronic money platforms in North Korea, not just in Pyongyang but across the entire country. For the state, electronic systems bring some efficiency to the economy, allow for price monitoring and control, and provide the data needed to collect taxes. The support of foreign currency in the network helps the state absorb hard cash in the economy, which can then be used by the state for its own business. Electronic payments can also add an additional layer of surveillance to the everyday lives of North Koreans, although the primary objective appears to be economic.